Subscribe to The COBRA Advisor newsletter for fresh HR insights, law updates, and more.

|

|

|

|

Employer responsibilities regarding HSAsEmployers offering HSAs do have certain responsibilities for both active employees and post-employment plan participants. This could encompass eligible actives, retirees, leave of absence personnel and COBRA or state continuation participants. Here's a simplified list of what you'll need to do to meet the employer obligations of Health Savings Accounts:

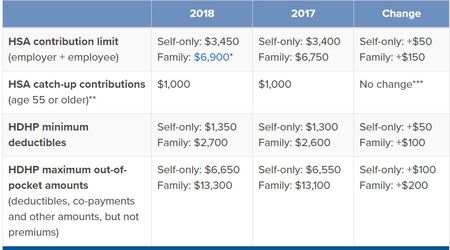

Benefits of Offering HSA paired with HDHPThere are some advantages for employers offering High Deductible Health Plans (HDHP) combined with HSA (Health Savings Account). An HSA program often offers flexibility as employers can be generous and fully fund the HSA and/or pay for the HDHP coverage. Employers may also choose to reduce their involvement in benefits by placing more responsibility on the employee. Consumer driven health care. The school of thought here (or at least that's how it once was) is that the employee (consumer) will be more careful and involved with his or her healthcare purchases if the employee is made to be responsible over the benefit (such as an HSA). The HSA combined with the health plan often increases the employees' desire to utilize the benefits (dollars) because it is their own money and they can keep unused money. Reduced premiums. High deductible health plans (keyword HIGH DEDUCTIBLE) are almost always less expensive than regular insurance plans. Less administrative responsibility. HSA's being savings accounts in the individual employees' control releases the employer from a great deal of administrative burden and benefits management. The employee in turn has more control over how and when the money is spent. A win, win. Employees like HSAs. While not all employees will understand the more complex details of their benefits, savvy employees who are informed of the benefits of having an HSA/HDHP will value this dynamic duo. You can learn more about helpful employee benefits information from our COBRA experts. 2018 HSA Limits:  For 2018, taxpayers with family coverage under an HDHP may treat $6,900 as the maximum deductible HSA contribution, up from $6,750 in 2017. Get Social With Us!

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Categories

All

Archives

May 2024

|

CONTACTCOBRA Help

1620 N High St Denver, CO 80218 Toll Free: (800) 398-2946 Local: (303) 322-2043 Email: [email protected] © Copyright 1986-2022 CobraHelp. All Rights Reserved

|

RESOURCES |

RESOURCES |

RESOURCESConnect with us!

|

RSS Feed

RSS Feed