Subscribe to The COBRA Advisor newsletter for fresh HR insights, law updates, and more.

|

|

|

|

There are numerous scenarios, life events, and COBRA events that work in conjunction with Medicare entitlement and eligibility, and employers must navigate these complex situations as they arise with a powerful combo of knowledge and resources. In this article we'll discuss several of the most commonly misunderstood issues related to Medicare and COBRA, and provide best practice insight for employers and brokers, no matter how large or small your company may be.

#1. My employee is enrolling in Medicare so we should cancel his active employee benefits, right?

No. An employee's Medicare entitlement does not mean that he or she should lose coverage as an active employee. In fact, employers who cancel active group health plan benefits for Medicare entitled employees may be subject to hefty fines and penalties. The Medicare Secondary Payer statute (MSP) 42 U.S.C. §1395y was enacted in 2003 to ensure that Medicare entitlement and benefits are secondary to employer plans when dealing with non-retirees. The exception to this is that employer groups with less than 20 employees. For small groups under 20 lives, Medicare pays first and the group health plan coverage becomes secondary. In other words, the employee gets to keep group health benefits even after he enrolls into Medicare.

MSP also includes a provision to ensure that employers cannot discriminate based on Medicare eligibility when it comes to offering coverage. That is, an employer cannot offer less coverage to those who may be entitled to Medicare benefits eligibility, while offering more coverage to other active employees who are not Medicare eligible. The only times that an active insured employee would lose group health coverage when he or she takes Medicare, is if that employee voluntarily waives the active group health plan coverage or if the employee experiences a COBRA qualifying event such as a termination of employment in conjunction with the Medicare entitlement. For more information, read CobraHelp’s information about Medicare Compliance. #2. If my former employee is Medicare eligible, doesn't that mean he does not qualify for COBRA?

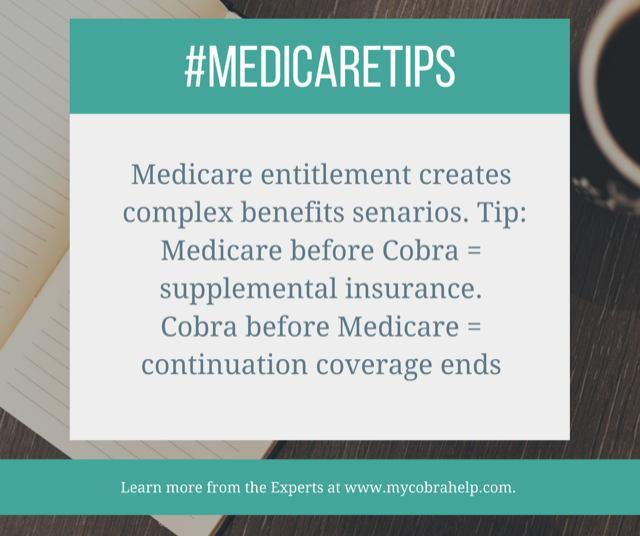

Contrary to popular belief, employees who are on Medicare prior to their COBRA qualifying event may be offered COBRA continuation coverage when a qualifying event occurs such as retirement (voluntary termination of employment). Under Federal COBRA, an employee is considered a qualified beneficiary when any COBRA qualifying event arises if he or she was enrolled into the group health benefits at the time of the qualifying event, regardless of Medicare benefits eligibility status. Thus, employees who are 65 (or older) and are group health plan participants at the time that a QE occurs, should be offered COBRA coverage just like anyone else who experiences a "termination of employment" event. In the latter situations, COBRA becomes secondary (or supplemental) insurance to Medicare.

Frequently, employees enroll in Medicare Part A because it is free, and wait for Part B until retirement. However, when the employee does this many plans will not pay for services when employees have coverage on plans that aren't covered under Medicare B. On the other hand, Medicare and COBRA law present us with a confusing flip-side to this scenario. That is, if the employee was enrolled in COBRA coverage before he became eligible for Medicare, then the COBRA participant would need to discontinue COBRA benefits once he becomes entitled (actively enrolled) into Medicare. The qualified beneficiary (or COBRA participant) cannot keep COBRA and take Medicare in the latter scenario. Most commonly, this happens when a COBRA participant turns 65 during his or her COBRA eligibility period of 18 months. #3. If my employee enrolls into Medicare, doesn't his spouse get 36 months of COBRA?

It depends. COBRA law tells us that a qualifying event by definition is a loss of coverage. The law also tells us that one type of "loss of coverage" (aka COBRA qualifying event) is when the Medicare Entitlement of the employee causes the spouse to lose coverage under the group health plan.

This type of loss of coverage typically occurs when the Medicare entitlement aligns with the COBRA event, such as retirement (voluntary termination of employment). When this happens, the employee's enrollment into Medicare paired with termination of employment, causes the spouse to lose coverage under the group health plan, and subsequently, the spouse is offered 36 months of COBRA continuation coverage. Now, that does not mean that there aren't other scenarios in which the employee's Medicare entitlement, subsequently entitles the spouse (or other dependents) to continue coverage under COBRA for a total of 36 months. It is always best to review the details of each situation, and make a determination based upon fact and the laws that pertain to COBRA and Medicare. Here are a couple of examples of how the spouse of an eligible employee could be eligible 36 months of COBRA:

For more questions about COBRA and Medicare compliance, call us today.

Resources:

Who Pays First - Guide for Employees and Employers to Medicare Benefits ECFR §54.4980B-7 Duration of COBRA continuation coverage Medicare.gov Guide Was this article helpful? For more information, follow us on:

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Categories

All

Archives

May 2024

|

CONTACTCOBRA Help

1620 N High St Denver, CO 80218 Toll Free: (800) 398-2946 Local: (303) 322-2043 Email: [email protected] © Copyright 1986-2022 CobraHelp. All Rights Reserved

|

RESOURCES |

RESOURCES |

RESOURCESConnect with us!

|

RSS Feed

RSS Feed